Auto loan delinquency is among the clearest indicators of overall consumer financial health. When household finances weaken, car payments are often among the first obligations to show stress.

| Key Auto Loan Delinquency Rates | |||||

| Period | Auto Loan 60+ DPD Rate | Prime 30+ DQ (Average) | Prime 60+ DQ (Average) | Subprime 30+ DQ (Average) | Subprime 60+ DQ (Average) |

| Q1 2025 Avg | 1.56% | ~1.80% | ~0.55% | ~15.3% | ~5.9% |

| Q2 2025 Avg | 1.49% | ~1.78% | ~0.55% | ~15.7% | ~5.8% |

| Q3 2025 Avg | 1.45% | ~1.97% | ~0.61% | ~17.0% | ~6.6% |

| Q4 2025 Avg | 5.21% | ~2.07% | ~0.63% | ~17.34% | ~6.66% |

| 2026 Outlook (Projected) | ~1.54% | 2.0% – 2.2% | 0.6% – 0.7% | 16.5% – 17.5% | 6.3% – 6.8% |

| Market sentiment | Positive | Stable to slightly rising | Stable | Stable but leveling | Elevated but contained |

The data points to a manageable but higher-risk environment in 2026. Overall delinquency is expected to stay near 2025 levels, but performance will continue to diverge by credit tier. Prime portfolios look relatively stable. Subprime portfolios remain pressured, with 30+ and 60+ day delinquencies likely to stay elevated.

While 2026 doesn’t look like a crisis year, it does look like a year where execution quality will separate strong portfolios from weak ones.

Auto Loan Delinquency Rates: Trends In 2026

Based on the data presented above, we’ve identified the following patterns, which represent key headwinds and tailwinds that will likely inform market trends over 2026:

| Key Auto Loan Delinquency Rates and Trends At a Glance | |||

| Trend | Primary Risk Signal to Monitor | Operational Lever That Moves the Needle | KPI to Track in 2026 |

| Delinquency Varies Sharply by Credit Tier | Subprime 60+ DPD vs. prime 60+ DPD spread | Tier-based underwriting rules and pricing floors | Delinquency gap by FICO band |

| Used Car Loans Show Higher Stress Than New | Used-vehicle early payment defaults | Tighter LTV/PTI caps on used inventory | 90-day default rate: used vs. new |

| Newer Vintages Underperform Older Cohorts | First-12-month delinquency by origination year | Adjust term limits and advance rates on new bookings | Vintage curve comparison (12-mo DPD) |

| Regional and Channel Differences Matter | State-level 30+ DPD and indirect-channel EPDs | Regional pricing grids and dealer segmentation | Delinquency by state and channel |

Trend 1: Delinquency Varies Sharply by Credit Tier

Not all borrowers are experiencing delinquency equally. Auto loan delinquency rates and trends now demonstrate a significant divide between higher-risk and lower-risk credit segments. Prime and super-prime borrowers continue to perform well, while subprime borrowers show disproportionately high delinquency rates, signaling where risk is most concentrated in auto portfolios.

What the data shows:

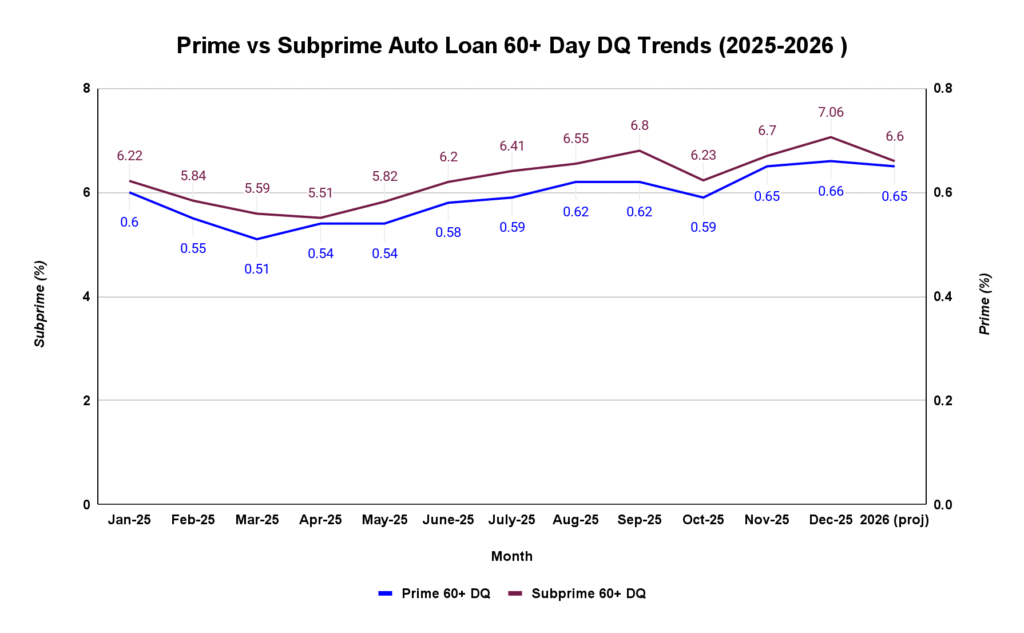

- Delinquency risk is highly concentrated in subprime portfolios: Throughout 2025, subprime 60+ day delinquency rates remained between roughly 5.5% and 6.8%, while prime borrowers stayed near 0.5%-0.6%, a gap of more than tenfold. Prime performance showed minimal month-to-month volatility, reflecting stronger borrower fundamentals.

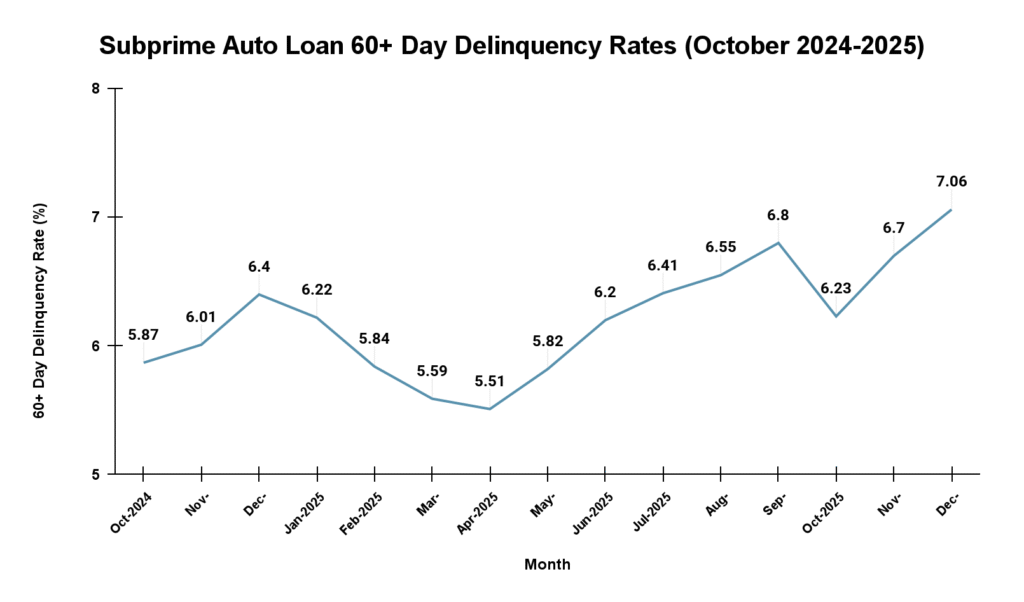

- Subprime delinquency remains elevated: Fitch Ratings subprime auto ABS performance data shows that 60+ day delinquency rates stayed persistently high throughout 2025, reaching 6.80% in September 2025 before easing slightly to 6.23% in October 2025. These levels remain materially above early-2024 readings and continue to signal concentrated stress in subprime auto portfolios.

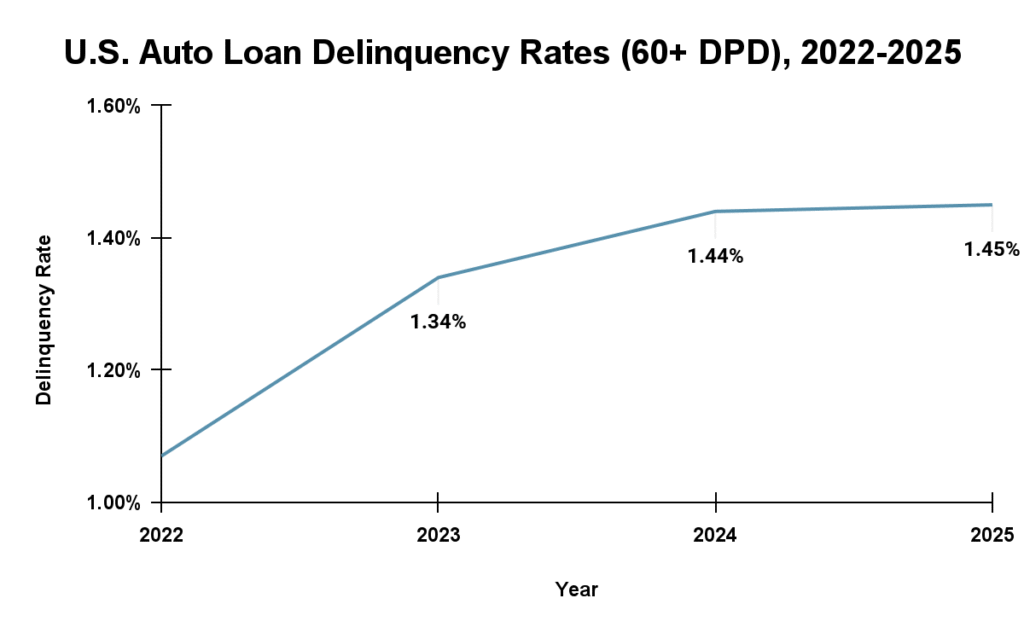

- Wider consumer-level delinquency trend: Overall auto loan 60+ DPD rates have been trending above historical norms, with the TransUnion industry insight showing consumer-level delinquency (60+ DPD) near ~1.45–1.56% across most of 2025, indicating persistent performance pressure even outside subprime segments.

What this means for lenders in 2026:

- Limited improvement expected in 2026: Forward estimates suggest prime delinquency will stay near current levels, while subprime performance is projected to remain elevated rather than meaningfully improve.

- Risk concentration: Lenders with high exposure to subprime borrowers will continue to face disproportionately higher delinquency and loss pressure compared with portfolios weighted toward prime and super-prime segments.

- Portfolio segmentation matters: Using broader metrics, such as overall delinquency, hides these divides. Focusing on tiered performance, especially within near-prime and below, lets lenders adjust underwriting, pricing, and risk limits more precisely.

- Dynamic credit strategy needed: In practice, lenders should build tier-based risk models that differentiate performance expectations, pricing structures, and collection strategies by segment-specific behavior rather than broad averages.

Trend 2: Used Vehicle Loans Show Higher Stress Than New

Performance in the auto market varies by vehicle type. Recent data indicate that used-vehicle loans are carrying higher payment burdens and performance risk compared with new-vehicle loans.

What the data shows

- Monthly payments differ meaningfully: According to the TransUnion Q3 2025 Credit Industry Insights Report, average monthly payments in Q3 2025 were $769 for new vehicles versus $538 for used vehicles, reflecting both higher prices and structural differences in financing.

- Overall delinquency remains elevated: The same TransUnion report shows the auto loan 60+ days delinquency rate at 1.45% in Q3 2025, up year-over-year, with used loans contributing more to performance pressure due to older collateral and tighter borrower cash flow.

- Collateral value and risk dynamics matter: Used vehicles typically depreciate faster and have lower average collateral values, which can amplify defaults when affordability weakens. This pattern is consistent with historical performance differentials across vehicle types.

What this means for lenders in 2026:

- Portfolio mix drives risk outcomes: Lenders with a higher share of used-vehicle financing should expect relatively higher delinquency pressures than those concentrated in new vehicles.

- Deal structure becomes essential: Controls such as term limits, loan-to-value (LTV) caps, and payment-to-income (PTI) thresholds are especially impactful for used loans, where equity cushions are thinner.

- Pricing must adapt to risk: Dynamic, segment-specific pricing helps compensate for higher volatility and performance risk in used-auto portfolios.

Trend 3: Newer Loan Vintages Are Underperforming Pre-Pandemic Benchmarks

Another defining pattern is that recently originated auto loans are showing weaker early performance than older vintages, particularly in near-prime and subprime tiers. This vintage effect is shaping how lenders evaluate risk and structure new originations.

What the data shows:

- Recent vintages show elevated early delinquency: TransUnion’s Q3 2025 Credit Industry Insights Report notes that delinquency rates among 2024 and 2025 auto loan vintages remain higher than comparable 2019 vintages, especially within prime-and-below risk tiers.

- Payment pressure is growing despite rate cuts: The same TransUnion analysis shows that average monthly payments for both new and used vehicles continued to rise in 2025, even as interest rates eased. Higher payment burdens have contributed to weaker performance in newer loans.

- Broader borrower stress reinforces the vintage effect: J.D. Power’s 2025 U.S. Automotive Financing Satisfaction Study reports that nearly 29% of auto finance customers are now categorized as financially vulnerable. While not a vintage metric directly, this rising borrower strain helps explain why newer cohorts are more sensitive to income shocks and more likely to fall behind early.

What this means for lenders in 2026:

- Not all delinquencies reflect long-term structural risk: Higher delinquencies among recent vintages do not necessarily indicate a permanently weaker borrower pool. Much of the underperformance is tied to loan structure and affordability conditions at origination (high prices, long terms, elevated payments).

- Vintage monitoring must drive credit strategy: Lenders need to evaluate performance by origination cohort, not just by credit score or portfolio averages. Comparing newer vintages to earlier years provides clearer insight into whether current underwriting and pricing remain appropriate.

- Underwriting guardrails matter more than ever: To protect newer vintages, lenders are increasingly:

- Reducing maximum advance rates

- Tightening payment-to-income thresholds

- Shortening allowable terms for higher-risk segments

- Pricing more aggressively for higher-LTV deals

- Reducing maximum advance rates

Trend 4: Regional and Channel Differences Are Creating Uneven Delinquency Pressure

Auto loan delinquency trends are not moving in lockstep across the market. Performance varies meaningfully by geography and by origination channel, with dealer-heavy portfolios and certain regions showing higher stress than others. This unevenness means national averages can mask localized pockets of risk that materially affect underwriting, pricing, and collections strategy.

What the data shows:

- Delinquency rates differ sharply by state and region: A recent state-level analysis shows large gaps in auto loan delinquency rates. As of early 2025, Mississippi (9.8%), Louisiana (8.4%), and Georgia (7.8%) had among the highest shares of borrowers with at least one delinquent auto loan, while states such as Utah, Washington, and New Hampshire were closer to 3%. These regional divides reflect differences in income levels, employment patterns, and borrower mix.

- Dealer-originated loans tend to show more volatility than direct channels: Industry performance studies consistently find that indirect (dealer-originated) portfolios exhibit greater dispersion in early payment defaults and delinquency transitions than direct-to-consumer channels. Dealer-heavy portfolios are more sensitive to shifts in used-vehicle values, borrower mix, and deal structure.

- Used-vehicle concentration amplifies regional risk: Markets with a higher share of used-vehicle financing, such as Mississippi, Louisiana, and Georgia, are experiencing greater delinquency pressure than markets weighted toward new vehicles. Higher loan-to-value ratios and longer terms in used deals are contributing to weaker performance in certain dealer-centric regions.

- Employment and cost-of-living differences are driving uneven outcomes: Areas with higher inflation-adjusted vehicle costs relative to median incomes are reporting higher late-payment rates, reinforcing that borrower affordability is increasingly a localized issue rather than a uniform national trend.

What this means for lenders in 2026:

Delinquency management cannot be addressed solely at the portfolio level. In 2026, effective lenders will manage risk with geographic and channel precision:

- Segment performance by region, not just credit tier: Lenders need state- and market-level dashboards that track approval rates, early delinquency, and collections outcomes separately by geography.

- Differentiate indirect and direct strategies: Dealer-originated portfolios require tighter controls around structure (LTV, term, PTI) and faster early-stage monitoring than direct channels, where borrower profiles are often more stable.

- Adjust pricing and terms by market conditions: Uniform national pricing grids are giving way to region-aware strategies that account for local risk dynamics.

- Align collections resources with hotspots: Early delinquency management should be concentrated in higher-risk markets rather than spread evenly across the portfolio.

Turning Auto Loan Delinquency Rates and Trends Insight Into Action

Managing modern auto loan portfolios requires systems that can detect risk earlier, segment it more precisely, and adjust automatically as conditions change. defi’s cloud-native origination and servicing platform, for example, helps lenders translate delinquency data into smarter, faster decisions by enabling:

- Real-time credit and pricing adjustments based on performance trends

- Dealer- and region-specific risk controls

- Automated stipulations and workflow management

- Early-warning analytics to spot emerging stress before it turns into loss

- Integrated servicing tools to respond quickly when accounts begin to slip

With defi SOLUTIONS, lenders gain the agility to manage risk with precision, while still delivering the speed and experience dealers and borrowers expect.

Ready to strengthen your portfolio for 2026? Book a demo to see how defi SOLUTIONS helps auto lenders improve credit execution, control delinquency risk, and operate more efficiently at scale.