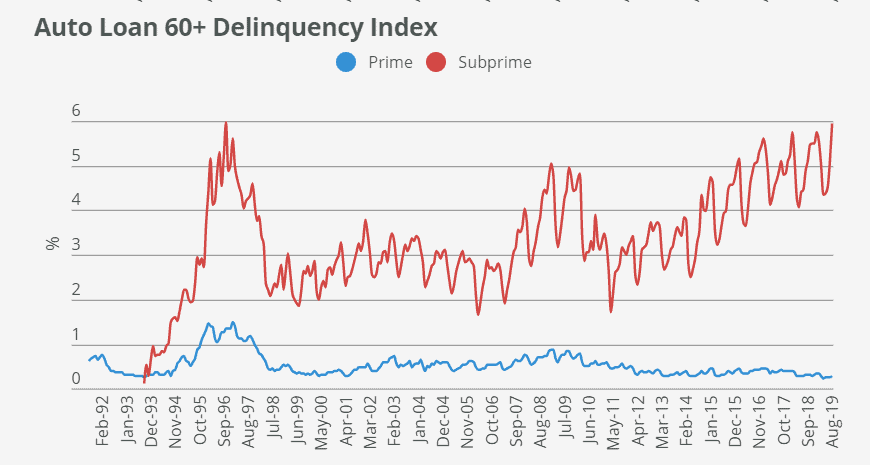

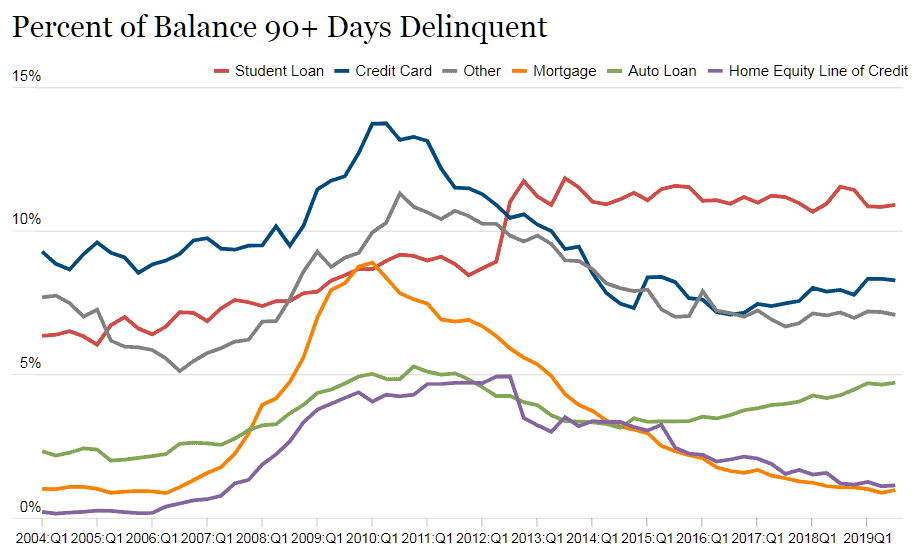

Looking at the two charts below, one could reasonably conclude that delinquency rates will likely continue their upward trend into 2020. Despite an economy that continues to roll along and a stock market setting new records, several factors are contributing to delinquencies in the subprime market and to auto loan balances now 90+ days delinquent.

- According to Experian, the average auto loan today ($32,119 for a new vehicle) is a third larger compared to a decade ago.

- Car prices increasing as a result of increasing instrumentation and digitization. This new technology has increased the price of even basic vehicles. Personal income growth now lags behind the rate of price increases.

- America aspires to own SUVs and tricked-out pickups with price tags well above that of the average sedan and sometimes their ability to pay.

- Loan terms can now exceed 72 months. Monthly payments seem low, while the total cost of the vehicle climbs. As a result, dealers are finding financing to be more profitable than vehicle sales.

With the increasing vehicle price tags, long-term payment plans that significantly add to vehicle costs, and stagnant wages that impact the subprime borrowers, the upward trend is not surprising.

Source: FitchRatings US Auto Indices

Want to find out more about our software and services? Contact our team today.

Source: Federal Reserve Bank of New York Household Credit and Debt Report

Source: Federal Reserve Bank of New York Household Credit and Debt Report

The impact of delinquencies depends upon market segment focus. Banks and credit unions with conservative credit policies experience minimum risk; however, some of these institutions are also now, taking on greater exposure than before. Fincos focused on the subprime segment—especially those that have seen write-offs increase as delinquency rates climb—may want to evaluate their current methods of assessing risk.

Consumer data, machine learning techniques, and predictive models are helping fincos carefully evaluate applicant credentials, propose risk-adjusted deals, and identify borrowers who are on the road to 90-day delinquency.

New Consumer Data and Analytics Reduce Lending Risk

Credit scores are the most direct means of assessing an applicant’s financial position. However, newer sources of data can paint a more detailed picture to help finco lenders better assess risk.

Alternative Credit Data aggregates consumer data such as utility and rental payments, bank accounts, employment history, real-estate, and cell-phone payments. With this additional data, finco lenders can more confidently assess an applicant’s creditworthiness.

Fraud Analysis identifies loan applications containing misrepresented information for the purpose of obtaining better terms, a vehicle of greater value, or outright vehicle theft by early payment defaults. Fraud analysis compares application information against machine learning algorithms to identify income and employment misrepresentation, false identity, straw buyers, and collateral inflation. Fraud analysis can be one of the most powerful techniques to reduce loan delinquency.

Machine Learning for Optimized Credit Models

Alternative data and fraud analysis help finco lenders reduce the risk of delinquency through better applicant qualification. Machine learning can also play a vital role in developing credit models. Using a wide range of data to evaluate risk, machine learning algorithms use hundreds of variables to assess applicant risk and propose deals that are fine-tuned to the applicant’s financial standing. Machine learning techniques give finco lenders an additional means of reducing delinquencies while simultaneously increasing approval rates.

Predictive Models Recognize Potential Delinquencies

Advanced analytical techniques help identify potential delinquencies. Analytics has the ability to analyze hundreds of variables and payment trends to develop predictive models that are fine-tuned to the unique market segments of the lender. Through continuous analysis of portfolio performance and borrower profile data, predictive models can correlate borrower attribute and payment behaviors to identify accounts headed for serious delinquency. With advanced notice of potential problems, automated workflows can guide representatives through a process designed to avoid delinquencies that lead to defaults.

Avoid Contributing to Auto Loan Delinquency Statistics in 2020

Finco lenders now have all the necessary tools and techniques available to help reduce their auto loan delinquency statistics in 2020. If you’re already contending with steadily increasing delinquencies, invest some time and evaluate the latest capabilities to help rein them in.

Getting Started

defi SOLUTIONS provides configurable loan origination systems, loan management and serving, analytics and reporting, and a wide range of technology-enabled BPO services. If you’re struggling with increasing delinquencies, we can help you reverse that trend. Contact our team today or register for a demo.