The demand for ATVs, UTVs, motorcycles, snowmobiles, and personal watercraft continues to accelerate as consumers prioritize outdoor recreation and manufacturers expand electric model lines.

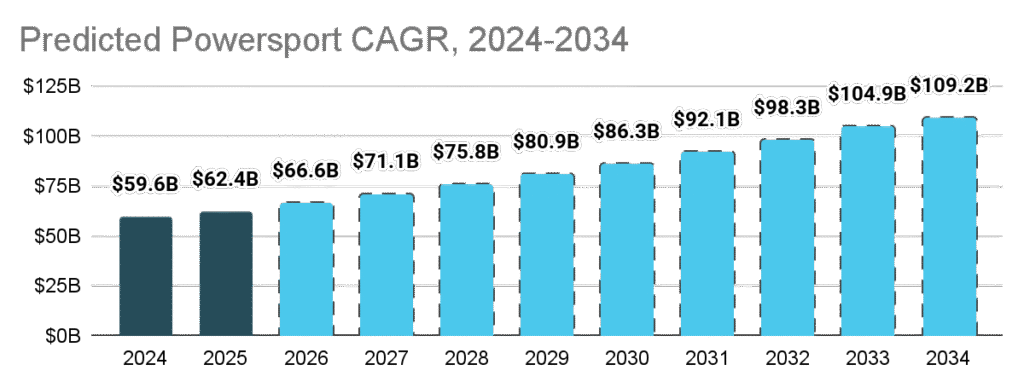

Currently valued at $62.4 billion, the global powersports market is projected to reach $109.2 billion by 2034, reflecting a 6.7% compound annual growth rate. This growth is opening the door for lenders to diversify portfolios, capture new yield, and strengthen performance in asset-backed lending.

At the same time, the segment brings unique challenges. Seasonal demand, shifting collateral values, and varied borrower profiles require more flexible systems. This article explains how powersport lending systems and servicing strategies help banks, credit unions, and captives streamline origination, manage risk, and maintain profitability through a mix of automation and outsourcing.

Automation vs. Outsourcing in Powersport Lending and Servicing

As the powersports market expands, lenders face an important choice: to build efficiency through automation or expand capacity through outsourcing. The right balance comes from aligning both strategies: automation to increase speed and accuracy, and outsourcing to scale efficiently as demand shifts.

1. Automation: Streamlining End-to-End Origination

Modern powersport lending systems allow lenders to digitize the entire loan lifecycle with minimal manual touchpoints. Configurable rules and integrations enable lenders to:

| Automation Focus Area | Primary Goal | Key Business Impact | Example in Powersport Lending |

|---|---|---|---|

| Underwriting Automation | Accelerate decisions | Cuts decision time from minutes to seconds | Auto-approve qualified borrowers with pre-set risk thresholds |

| Workflow Standardization | Reduce variance | Improves policy consistency and auditability | Same lending criteria applied across all dealer channels |

| Data Integration | Strengthen decision quality | Creates complete borrower profiles | Combines credit, collateral, and income data from multiple sources |

| Scalable Infrastructure | Maintain efficiency at volume | Avoids overtime and staffing costs | Handles seasonal loan surges without expanding the team |

2. Outsourcing: Scaling Servicing and Resource Efficiency

Powersport lending servicing, which involves payment processing, collections, and customer support, is just as resource-intensive. Through partnering with an outsourced servicing provider, lenders gain:

| Outsourcing Focus Area | Primary Goal | Key Business Impact | Example in Powersport Lending |

|---|---|---|---|

| Variable Cost Model | Convert fixed costs to flexible operating expenses | Improves margin control and scalability | Pay only for active loan volume instead of maintaining full-time servicing teams |

| Specialized Expertise | Access experienced servicing professionals | Enhances borrower experience and regulatory accuracy | Teams trained in short-term, seasonal repayment cycles and collateral-specific nuances |

| Operational Continuity | Maintain service levels amidst demand fluctuations | Reduces borrower disruption and delinquency risk | Support remains stable during off-season slowdowns or high-volume periods |

| Strategic Focus | Reallocate resources to high-value initiatives | Strengthens dealer and portfolio strategy | Frees employees to focus on dealer partnerships and growth opportunities |

Automation vs. Outsourcing: Pros and Cons for Powersport Lenders

No two lenders manage powersport portfolios the same way. While powerful lending systems and outsourced servicing both improve efficiency, each approach has its own advantages and limitations, depending on your resources, portfolio mix, and growth goals.

| Approach | Pros | Cons |

|---|---|---|

| Automation – LOS | Accelerates decisioning and funding through rule-based workflows Reduces manual data entry, improving accuracy and compliance Integrates directly with dealer systems and credit bureaus Provides transparency through dashboards and real-time reporting | Requires upfront investment and integration time Still needs human oversight for exceptions or non-standard applications since ROI depends on volume; less impactful for low-loan environments |

| Outsourced Servicing | Converts fixed operational costs into variable ones Provides immediate scalability during peak seasons Access to trained servicing experts and borrower support teams Improves consistency in payment processing, collections, and compliance | Less direct control over day-to-day borrower interactions Requires clear SLAs and data-sharing protocols Quality depends on vendor alignment and technology integration |

Finding the Right Balance

Many lenders combine both strategies. They use powersport lending systems for automating origination, and servicing partners for handling post-funding tasks.

Together, these solutions help:

- Reduce cost per origination by up to 40%

- Reduce the time it takes to originate a loan by up to 50%

- Cut operations time by 30-40%, freeing staff for higher-value tasks such as dealer support and complex underwriting

- Achieve improved compliance accuracy through standardized workflows and oversight

- Prevents 40-60% of early payment defaults linked to fraud schemes

By aligning these solutions to your portfolio strategy, you can expand profitably without compromising service quality or compliance integrity.

How Powersport Lending Systems and Servicing Shape Profitability Across Lender Types

Every lender enters the powersports market with a different foundation. Whether you’re a captive lender, bank, or credit union, the mix of automation and servicing you choose directly affects your cost structure, risk exposure, and borrower experience.

| Lender Type | How Automation Helps | How Outsourcing Helps | Profit Impact |

|---|---|---|---|

| Captive Lenders | Streamlines dealer-driven intake | Ensures consistent borrower servicing | Faster funding and higher dealer satisfaction |

| Banks | Extends auto workflows to powersports | Converts fixed costs to variable | Lower overhead and controlled growth |

| Credit Unions | Delivers fast, transparent member experience | Adds coverage during peaks and after-hours | Stronger retention and competitiveness |

Captive Lenders

Captive finance companies already operate within tightly integrated dealer networks, but scaling profitably requires systems that can keep pace with fluctuating application volume.

Automation helps by streamlining dealer-driven intake, reducing delays caused by manual routing or verification gaps. Outsourcing complements this by ensuring consistent borrower communication and payment handling, even during peak sales periods.

Together, these capabilities shorten loan-to-funding cycles, strengthen dealer satisfaction, and help captives maintain a consistent brand experience without expanding internal servicing teams.

Banks

For banks, powersport lending is often a diversification strategy. But legacy systems can slow expansion into new vehicle types. Automation solves this by extending existing auto workflows to powersport products with minimal disruption, allowing banks to add new asset classes efficiently.

Outsourcing converts what would otherwise be fixed operational costs into variable ones, enabling banks to manage niche portfolios without building new internal divisions. This combination can reduce overhead, improve ROA, and support controlled, profitable entry into the powersports market.

Credit Unions

Credit unions must balance member service with the need to modernize lending operations. Automation gives members the fast, transparent experience they expect, while still supporting the personalized service credit unions prioritize.

Outsourcing adds after-hours coverage and seasonal capacity, preventing service gaps when team availability is limited. These gains result in smoother borrower experiences, higher satisfaction, and stronger member retention, ultimately allowing credit unions to stay competitive with larger lenders in the growing powersports segment.

The Road Ahead: Smarter Systems, Stronger Servicing

The powersports market is expanding fast, and lenders that move first stand to capture the most value. But success requires the right technology infrastructure and operational model to originate, fund, and service loans efficiently.

Modern powersport lending systems and servicing solutions give lenders the edge to compete:

- Automation accelerates application throughput, standardizes workflows, and ensures compliance from day one.

- Outsourcing reduces fixed overhead, improves responsiveness, and helps keep portfolios profitable even during seasonal volume swings.

Together, these solutions form a connected ecosystem that helps captives, banks, and credit unions scale intelligently.

Learn how defi’s integrated systems and servicing can help your organization improve efficiency, strengthen borrower relationships, and grow confidently in the powersports market.

Frequently Asked Questions for Powersport Lending Systems and Servicing

What is powersport lending?

Powersport lending refers to financing for recreational and utility vehicles such as ATVs, UTVs, motorcycles, snowmobiles, and PWCs. These loans often involve seasonal demand, unique collateral types, and varied borrower profiles, which is why lenders rely on specialized systems and servicing models to manage risk and maintain profitability.

How much does powersport lending automation cost?

The cost of powersport lending automation varies widely, depending on factors such as loan volume, complexity, integrations, and whether servicing is included. Typical industry ranges look like:

- Small to mid-sized lenders (<10,000 loans/year): Cloud LOS implementations typically range from $150,000 to $400,000 in the first year, depending on configuration needs and integration requirements.

- Mid-to-large lenders (10,000–100,000+ loans/year): Large-scale deployments that include LOS and servicing workflows, as well as multiple integrations, typically range from $500,000 to $2 million or more over the first 1–3 years.

- Enterprise lenders: Multi-state, multi-product deployments with deep integrations, complex risk models, and high-volume servicing can exceed $3 million–$5 million over multi-year programs.

These ranges reflect typical market benchmarks across lending technology providers. Because each lender’s portfolio, systems, and operational goals differ significantly, the most accurate way to obtain numbers is through a tailored assessment with the vendor.

Should credit unions outsource powersport loan servicing?

Yes, outsourcing can be a strong option for credit unions, especially those expanding into powersport lending without large servicing teams.

A servicing partner brings specialized expertise with niche collateral, offers variable-cost scalability during seasonal volume swings, and maintains consistent borrower support. It also frees internal staff to focus on member relationships, underwriting, and program growth.

The key is choosing a provider that aligns with your service standards and integrates smoothly with your lending systems.

defi SOLUTIONS is redefining loan origination with software solutions and services that enable lenders to automate, streamline, and deliver on their complete end-to-end lending lifecycle. Borrowers want a quick turnaround on their loan applications, and lenders want quick decisions that satisfy borrowers and hold up under scrutiny. For more information on powersport lending systems and servicing, Contact our team today and learn how our cloud-based loan origination products can transform your business.