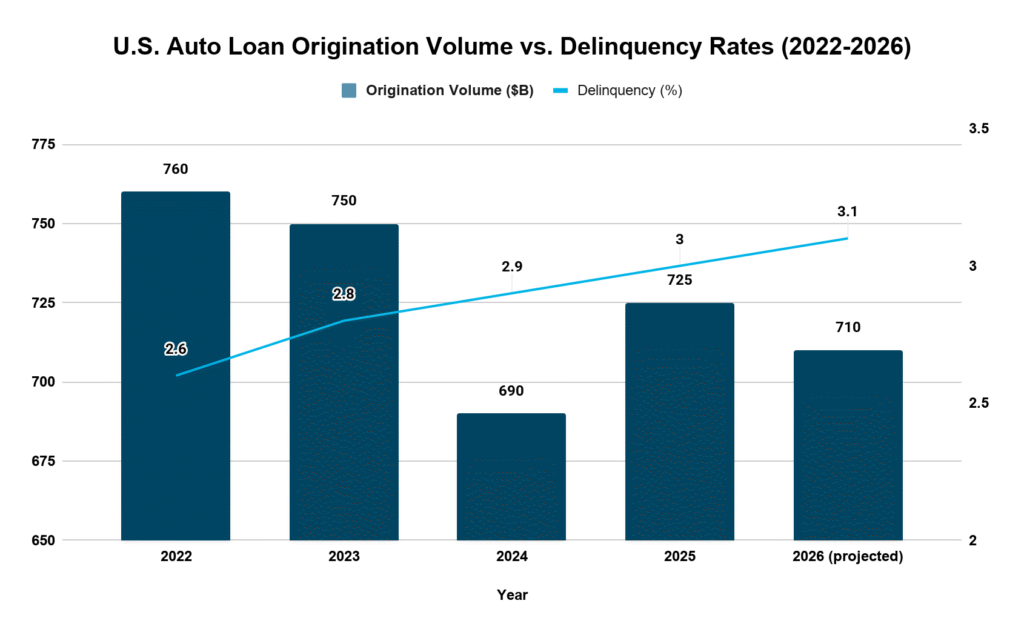

U.S. auto lending remains elevated, with origination volumes consistently in the $700 to $750 billion range over the past several years. At the same time, delinquency rates have steadily increased, rising from roughly 2.6% in 2022 to around 3.0% and above in recent periods.

For lenders, this means handling large volumes of applications while applying tighter oversight to underwriting, fraud detection, and funding decisions.

A digital lending process helps lenders manage this balance by structuring validation, decisioning, documentation, and funding into a coordinated workflow. This article explains why that capability has become essential for auto lenders.

Where Traditional Digital Lending Process Workflows Break Down, and How to Fix Them

Most lending processes were built incrementally. Over time, adding vendors, manual checkpoints, and compliance safeguards introduces friction that compounds across the workflow. What begins as isolated inefficiencies becomes systemic delay, slowing decisions, increasing costs, and limiting scale.

These breakdowns tend to occur in predictable places, and the delays they create are a function of how the process is built, not how hard the team works.

*Figures represent estimated workflow timing based on typical manual and digital lending process benchmarks.

In manual environments, tasks that take 16 to 48 hours can often be reduced to minutes in digitally orchestrated workflows, compressing timelines across every stage of the lending process.

The sections below highlight where delays occur, what causes them, and structural fixes.

Queue dependency

When every application enters a manual review queue, turnaround time becomes tied to staffing levels and business hours. Peak submission periods create backlogs that translate directly into dealer dissatisfaction.

- How to fix it: Configure policy-based decision rules so routine, in-policy applications move automatically, reserving underwriter review for exceptions. Average decision time shortens without adding headcount.

Disconnected systems

Credit data, income verification, fraud checks, document generation, and servicing platforms often operate independently, which means someone is rekeying data or manually reconciling outputs between steps.

- How to fix it: Integrate these tools directly into the origination workflow via APIs. When data moves automatically between systems, errors decrease, and funding cycles shorten.

Late-stage validation

Identity inconsistencies, income discrepancies, and collateral issues that surface after conditional approval force rework at the worst possible point in the process.

- How to fix it: Run identity, income, and valuation checks at submission. Catching issues early reduces downstream exceptions and improves confidence in the approval before it is issued.

Limited operational visibility

When managers can only see aging files or pipeline bottlenecks in periodic reports, problems are already affecting funding timelines before anyone acts on them.

- How to fix it: Deploy real-time dashboards that surface pipeline status, decision speed, and exception rates. Visibility allows course correction before delays reach dealers or borrowers.

None of these fixes requires reinventing underwriting. They require restructuring how the workflow operates so that speed and control coexist rather than trade off against each other.

What to Evaluate When Building a Digital Lending Process

Not every platform labeled “digital” fundamentally changes how origination performs. A strong digital lending process should meet measurable standards in the areas below.

1. Decision Logic and Policy Configuration

Credit score bands, LTV limits, PTI/DTI thresholds, term caps, and pricing adjustments should be configurable directly within the platform so lenders can adjust policy as lending conditions change.

| Evaluation Area | What to Evaluate | What Strong Looks Like |

| Decision Logic & Policy Configuration | Ability to configure: Credit score bands LTV limits PTI / DTI thresholds Term caps Pricing adjustments | Internal rule updates (no vendor dev required) Changes deploy in hours or days Rules apply across all channels 60%–80% of routine approvals automated |

When policy logic is fully embedded in the origination workflow, routine approvals can move automatically while underwriters focus on exceptions. If underwriters are still reviewing standard approvals simply to confirm policy compliance, the policy engine is likely not fully integrated.

2. Real-Time Data Integrations

A digital lending process depends on real-time access to borrower and collateral data. Credit bureau information, identity verification, income validation, fraud signals, and collateral values should be integrated directly into the application workflow so lenders can evaluate risk immediately at submission.

| Capability | What to Evaluate | What Strong Looks Like |

| Real-Time Data Integrations | Integration of: Credit bureau data Identity verification Income validation Fraud detection Collateral valuation | Credit pulls and validation in seconds Identity and income checks run at submission New data providers added without major redevelopment <15%–20% of files require manual data gathering |

When verification tools run automatically at submission, lenders can evaluate risk signals before a credit decision is issued. If lending must gather income documents, identity checks, or collateral values manually, the process remains partially digitized rather than fully digital.

3. Exception Management

A digital lending process should narrow the focus of underwriting teams to the deals that truly require human judgment. Applications that fall outside policy thresholds should be routed automatically and presented with the relevant risk signals already identified.

| Evaluation Area | What to Evaluate | What Strong Looks Like |

| Exception Management | How out-of-policy deals are routed and presented to underwriters | Exceptions tagged with risk indicators (high PTI, high LTV) Key risk data surfaces immediately Exception queues represent a minority of the total volume Review time per exception reduced |

When exception management is structured properly, underwriters can focus on complex credit scenarios rather than assembling data to understand why a deal triggered review.

4. Document and Funding Workflow

Once a loan is approved, documentation and funding should move forward automatically without requiring separate systems or manual coordination. A digital lending process integrates stipulation management, document generation, and electronic signature workflows directly within the origination platform.

| Evaluation Area | What to Evaluate | What Strong Looks Like |

| Document & Funding Workflow | Whether approvals trigger automated documentation and funding steps | Stipulations generate automatically from policy gaps Documents auto-populate from application data Borrowers complete e-signatures within the same workflow Funding cycle time reduced by 1–3 days |

When documentation workflows are embedded within the origination platform, the gap between approval and funding narrows significantly. If lenders rely on external systems or manual document preparation, delays and deal fallout often persist.

5. Operational Visibility

As origination volume increases, leadership needs real-time visibility into pipeline performance and portfolio risk indicators. A digital lending process should provide continuous insight into how applications move through the pipeline and where operational bottlenecks occur.

| Evaluation Area | What to Evaluate | What Strong Looks Like |

| Operational Visibility | Ability to monitor pipeline health and performance metrics | Live dashboards for application aging and turnaround time Approval, capture, and funding ratios by dealer and channel Exception rates tracked by credit tier Early delinquency tied to origination attributes |

Without this level of visibility, lenders may scale application volume without understanding where performance gaps or risk concentrations are developing. Real-time operational insights allow leadership to adjust strategy before small issues become portfolio-wide problems.

6. Compliance and Audit Controls

Regulatory expectations require lenders to document how credit decisions are made and which rules were applied at the time of approval. A digital lending process should automatically log policy applications and maintain a clear audit trail.

| Evaluation Area | What to Evaluate | What Strong Looks Like |

| Compliance & Audit Controls | Whether rule application is logged and version-controlled | Every decision tied to the active rule set Policy updates are archived and traceable Fair lending reporting is generated automatically Audit preparation completed in days rather than weeks |

When compliance controls are embedded in the lending platform, lenders can demonstrate how decisions were made without having to manually reconstruct the process. If audit preparation requires assembling data across multiple systems, compliance risk and operational burden increase.

Turning Digital Structure Into Operational Performance

Designing a digital lending process requires structuring decision logic, validation, documentation, compliance controls, and reporting into a single coordinated environment.

defi ORIGINATIONS was built to unify those components inside one platform. Configurable decision rules, real-time data integrations, automated stipulations, document workflows, and audit tracking operate within the same structured process. Lenders can adjust credit strategy, monitor performance, and manage risk without rebuilding infrastructure each time market conditions shift.

Book a demo with defi SOLUTIONS to see how a unified digital lending process supports scalable, resilient auto lending.