Auto lenders originate loans in two primary ways: direct auto lending and indirect auto lending.

Both models can be profitable, both can scale, and both carry very different operational, risk, and technology requirements. The table below provides a high-level summary of the differences between the two:

| Direct vs. Indirect Auto Lending: At a Glance | ||

| Dimension | Direct Auto Lending | Indirect Auto Lending |

| Who originates the loan | Borrower applies directly to the lender | Dealer originates and assigns to lender |

| Primary channel | Website, branches, call center | Dealership finance office |

| Customer relationship | Owned by lender | Primarily owned by dealer |

| Speed at point of sale | Slower for car purchase | Faster for the buyer |

| Competition | Competes with other lenders online | Competes inside the dealership |

| Cost to acquire | Higher marketing costs | Dealer compensation costs |

| Deal structure control | High | Shared with dealer |

| Data visibility | Cleaner, lender-controlled | Dependent on dealer inputs |

| Volume scalability | Gradual | Can scale rapidly |

| Typical risk profile | More consistent | More variable |

With these differences in mind, this guide compares direct vs. indirect auto lending across the factors that matter most: cost, speed, risk, compliance, borrower experience, and growth potential, to help lenders choose the right medium for loan origination.

Who Originates the Loan

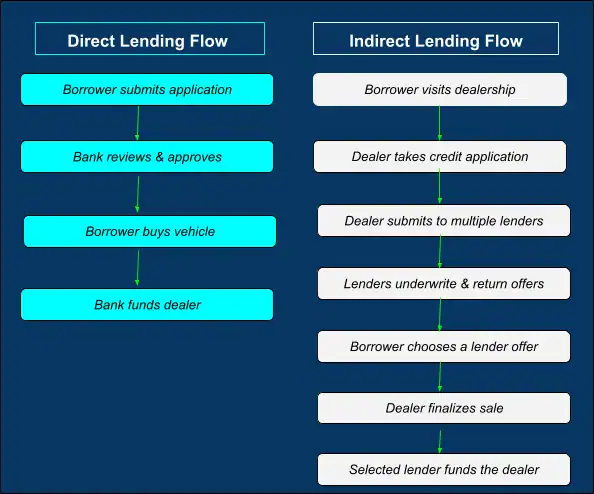

The simplest way to differentiate between direct and indirect auto lending is in how they actually function. The diagram below outlines the lending flow process for both:

- In direct lending, the lender originates the loan directly with the borrower. For example, consider a customer who applies for an auto loan on a bank’s website, gets approved, and walks into the dealership with pre-approved financing already in hand.

- With indirect lending, the dealer originates the transaction at the point of sale and sends it to the lender. This would be like if that same borrower instead sat in the dealership finance office, completed a credit application, and the dealer submitted it to multiple lenders for approval.

Origination ownership shapes the entire workflow; in direct lending, the lender controls the experience from day one. In indirect auto lending, the dealer controls the front end, and the lender’s role begins after the deal is already in motion.

Primary Channel

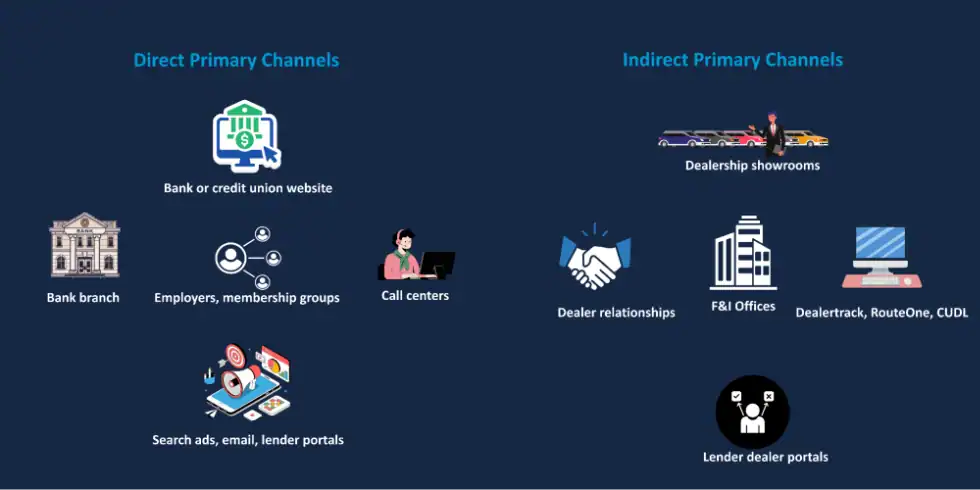

It’s also important to consider what pathways each lending model uses to bring in loans:

- Direct lending: Loans flow through lender-owned channels. This could be a credit union that runs Google ads promoting “auto loan preapproval in minutes,” and funds deals directly from its website.

- Indirect lending: Loans flow almost entirely through dealerships and dealer platforms. The borrower typically chooses the vehicle first and the lender second.

The channel dictates what kind of organization you need. Direct lending requires strong consumer marketing and digital experiences. Indirect lending requires dealer relationships, integrations, and fast point-of-sale execution.

Customer Relationship

Beyond where loans come from, the two models create very different kinds of borrower relationships. Who “owns” the customer experience has major implications for loyalty, cross-sell potential, and long-term value.

- Direct lending: The relationship is owned by the lender from day one. The borrower interacts only with the bank for approval, funding questions, and servicing. This often leads to stronger cross-sell opportunities, a higher likelihood of repeat business, and more loyalty over time.

- Indirect lending: In this, the dealer owns the front-end relationship, while the lender owns the back-end relationship. The customer may feel loyal to the dealership but not necessarily to the lender that ultimately funded the loan.

Direct lending creates deeper, longer-lasting borrower relationships that lenders can grow and monetize over time. Indirect lending, by contrast, prioritizes dealership relationships and transaction flow. One model builds customer equity for the lender; the other builds channel equity through the dealer network.

Speed at the Point of Sale

Timing plays a very different role depending on the channel. In one model, speed is helpful; in the other, it’s often the deciding factor.

- Direct lending: Speed is important, but not urgent. Borrowers are often comparison shopping and can tolerate a bit more back-and-forth.

- Indirect lending: Speed is mission-critical here. At a dealership, the borrower is ready to buy, while other lenders are competing for the same deal, and delays can mean losing the sale.

Indirect lending demands real-time decisioning, automated stipulations, and near-instant funding workflows. A lender that’s even slightly slower could lose volume quickly.

Competition

Direct and indirect lenders win business in entirely different ways, and at very different stages of the borrower journey.

- Direct lending: You compete for the borrower’s attention before they choose a vehicle. The borrower could be comparing rates on your website, at their local credit union, and with an online fintech before deciding.

- Indirect lending: You compete with other lenders for the same transaction while the borrower is sitting at the dealership. The decision often comes down to approval certainty, dealer experience, funding speed, and ease of doing business.

Direct lending competition is largely marketing-driven, won through brand, digital experience, and rate positioning early in the shopping journey. Indirect lending competition is primarily execution-driven, won in real time through fast decisions, strong dealer relationships, and seamless funding.

Cost to Acquire

Cost to acquire refers to the costs associated with obtaining new customers, whether through marketing or other channels. Lenders experience varied costs depending on which model they decide to use:

| Channel | Cost Range | Annual Acquisition Spend (10,000 loans per year) |

| Direct Lending | $230–$455* | $2.3M – $4.55M |

| Indirect Lending | $125–$275* | $1.25M – $2.75M |

*Estimates reflect typical industry ranges for U.S. auto lenders. Actual acquisition costs vary based on credit tier, marketing strategy, dealer incentive structures, and operating model.

- Direct lending: You pay to find every borrower yourself. Ads, call centers, and consumer acquisition drive the majority of the cost.

- Indirect lending: The dealer brings the customer, so acquisition costs are lower, but you spend more on dealer incentives, integrations, field reps, and program support.

Direct lending generally produces higher lifetime value and stronger brand ownership, but at a higher upfront acquisition cost. Indirect lending typically delivers lower per-loan acquisition expense, but requires ongoing investment in dealer relationships and execution infrastructure.

Deal Structure Control

The presence, or absence, of a dealership intermediary changes how much influence the lender has over the final deal.

- Direct lending: The lender controls everything, including rate, term, LTV, product mix, and add-ons. There is no intermediary influencing the structure.

- Indirect lending: Dealers have significant influence over markups, product add-ons, vehicle selection, and loan structure changes. Lenders must enforce controls programmatically rather than conversationally.

Direct lending gives lenders full, hands-on control over deal structure. Indirect lending requires the same controls to be enforced through systems, rules, and automation rather than through direct borrower interaction.

Data Visibility

Data quality and transparency are shaped by who controls the workflow. The more steps that pass through third parties, the more challenging consistent visibility becomes.

- Direct lending: Data is cleaner and more consistent because the lender controls the entire workflow from application to funding. With first-party borrower data, you know exactly how the shopper found you, what offers they saw, and every step of their application journey.

- Indirect lending: Data comes from multiple dealer systems and users, which can create inconsistent inputs, re-keying, and variability in deal quality.

In direct lending, data visibility is a built-in advantage. In indirect lending, it’s an operational challenge that must be engineered. Lenders that invest in orchestration layers, validation rules, and dealer data standards can close the gap, but it requires deliberate infrastructure.

Volume Scalability

Growth mechanics differ sharply between the channels. One scales gradually through borrower acquisition, while the other can scale rapidly through distribution partnerships.

- Direct lending: Growth is steady but incremental. Scaling requires more marketing, more employees, and greater borrower outreach efforts. To double volume, you may have to double the ad spend, branch activity, or partnership efforts.

- Indirect lending: Volume can scale quickly by adding new dealer relationships, expanding approvals, and improving turn times. A single large dealer group can materially change monthly originations.

Direct lending scales one borrower at a time. Indirect lending scales one dealership at a time. That difference makes indirect channels far more powerful for accelerating originations, but also more sensitive to execution quality and dealer experience.

Typical Risk Profile

Because the channels attract different kinds of borrowers, they also produce meaningfully different risk profiles.

- Direct lending: Portfolios often skew toward prime borrowers, since those who proactively shop for financing tend to have stronger credit and more predictable performance.

- Indirect lending: A dealer-oriented portfolio may include higher-risk segments, such as near-prime and subprime borrowers seeking immediate financing.

Direct lending is generally a lower-variance, prime-oriented strategy. Indirect lending is a higher-variance, distribution-driven strategy. The broader risk spectrum in indirect portfolios creates opportunities for volume, but it also requires tighter risk management, faster feedback loops, and more active credit management.

How to Decide Between Direct and Indirect Auto Lending

The right model depends on how you want to acquire borrowers, how fast you need to scale, and how much control you want over the customer relationship.

Here are some questions to guide your direct vs. indirect auto lending decision:

| Key Questions | If “Yes,” Lean Toward… |

| Do you want to own the borrower relationship from day one? | Direct |

| Is clean, first-party data critical to your strategy? | Direct |

| Do you want full control over loan structure and add-ons? | Direct |

| Do you prefer a more prime-focused, predictable portfolio? | Direct |

| Is keeping acquisition cost as low as possible a priority? | Indirect |

| Can your systems handle real-time dealer integrations? | Indirect |

| Is rapid portfolio growth more important than brand ownership? | Indirect |

| Are you comfortable managing higher risk tiers? | Indirect |

In practical terms:

- Choose direct lending if your goal is long-term customer value, cleaner data, tighter credit control, and stronger brand ownership.

- Choose indirect lending if your priority is fast volume growth, lower acquisition costs, and dominating transactions at the point of sale.

Most successful lenders ultimately use both channels, treating direct lending as a relationship engine and indirect lending as a growth engine.

When a Hybrid Strategy Makes the Most Sense

Many lenders don’t need to pick just one. A hybrid approach often works best:

- Use indirect lending to acquire new borrowers at scale

- Use direct lending for refinances, repeat customers, and cross-sell

- Let each channel play to its strengths

This structure allows you to grow volume through dealerships while still building long-term customer relationships on the back end.

Choosing the Right Channel Starts With the Right Platform

Whether you pursue direct lending, indirect lending, or a hybrid of both, one truth stays constant: your strategy can only scale as far as your technology allows.

Direct channels demand seamless digital experiences, fast credit decisions, and clean integrations with consumer-facing tools. On the other hand, indirect channels require real-time dealer connectivity, automated decisioning, and reliable funding workflows.

With direct vs. indirect auto lending, execution is the differentiator.

That’s where defi SOLUTIONS can help.

defi delivers a unified platform that supports the full spectrum of auto lending; direct, indirect, and everything in between. With configurable decisioning, dealer integrations, real-time orchestration, and end-to-end servicing capabilities, defi helps lenders compete effectively in whichever channel fits their strategy.

Book a demo to see how a modern lending platform can power your strategy, no matter which channel you choose.